Sold For $3,086

*Includes Buyers Premium

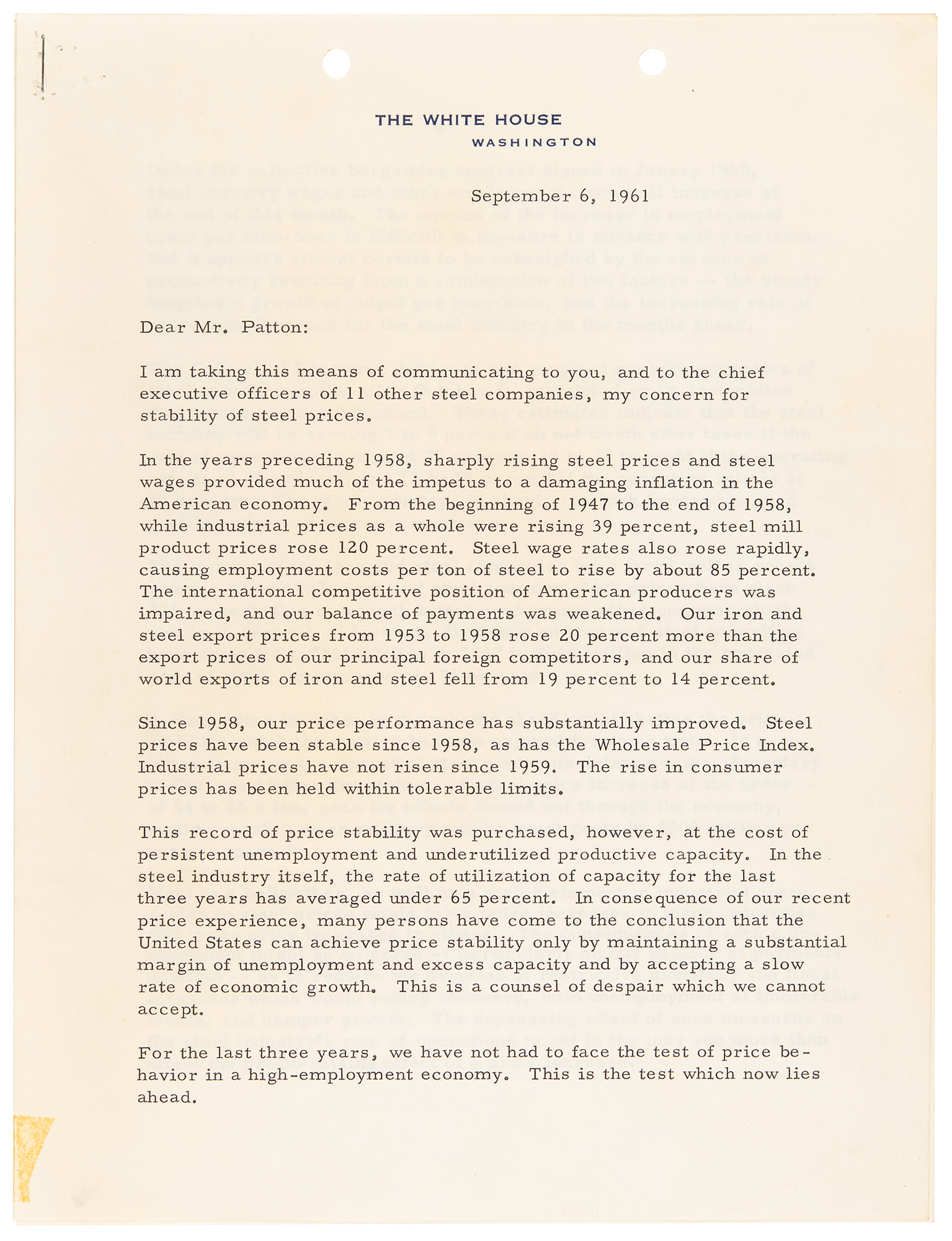

TLS as president signed “John Kennedy,” three pages, 8 x 10.5, White House letterhead, September 6, 1961. Lengthy letter to Thomas F. Patton, president of the Republic Steel Corporation, in full: “I am taking this means of communicating to you, and to the chief executive officers of 11 other steel companies, my concern for stability of steel prices.

In the years preceding 1958, sharply rising steel prices and steel wages provided much of the impetus to a damaging inflation in the American economy. From the beginning of 1947 to the end of 1958, while industrial prices as a whole were rising 39 percent, steel mill product prices rose 120 percent. Steel wage rates also rose rapidly, causing employment costs per ton of steel to rise by about 85 percent. The international competitive position of American producers was impaired, and our balance of payments was weakened. Our iron and steel export prices from 1953 to 1958 rose 20 percent more than the export prices of our principal foreign competitors, and our share of world exports of iron and steel fell from 19 percent to 14 percent.

Since 1958, our price performance has substantially improved. Steel prices have been stable since 1958, as has the Wholesale Price Index. Industrial prices have not risen since 1959. The rise in consumer prices has been held within tolerable limits.

This record of price stability was purchased, however, at the cost of persistent unemployment and underutilized productive capacity. In the steel industry itself, the rate of utilization of capacity for the last three years has averaged under 65 percent. In consequence of our recent price experience, many persons have come to the conclusion that the United States can achieve price stability only by maintaining a substantial margin of unemployment and excess capacity and by accepting slow rate of economic growth. This is a counsel of despair which we cannot accept.

For the last three years, we have not had to face the test of price behavior in a high-employment economy. This is the test which now lies ahead.

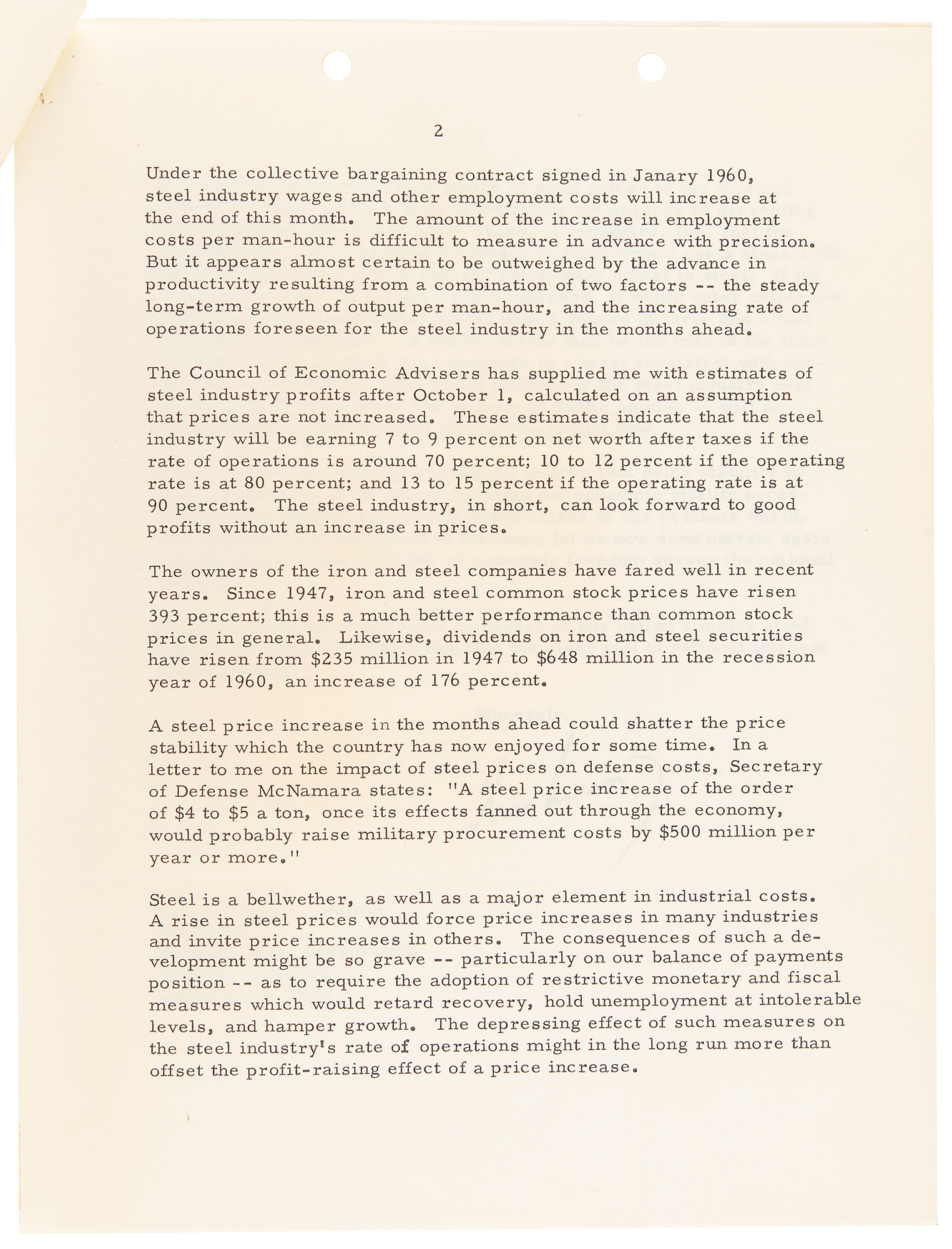

Under the collective bargaining contract signed in January 1960, steel industry wages and other employment costs will increase at the end of this month. The amount of the increase in employment costs per man-hour is difficult in advance with precision. But it appears almost certain to be outweighed by the advance in productivity resulting from a combination of two factors – the steady long-term growth of output per man-hour, and the increasing rate of operations foreseen for the steel industry in the months ahead.

The Council of Economic Advisers has supplied me with estimates of steel industry profits after October 1, calculated on an assumption that prices are not increased. These estimates indicate that the steel industry will be earning 7 to 9 percent net worth after taxes if the rate of operations is around 70 percent; 10 to 12 percent if the operating rate is at 80 percent; and 13 to 15 percent if the operating rate is at 90 percent. The steel industry, in short, can look forward to good profits without an increase in prices.

The owners of the iron and steel companies have fared well in recent years. Since 1947, iron and steel common stock prices have risen 393 percent; this is a much better performance than common stock prices in general. Likewise, dividends on iron and steel securities have risen from $235 million in 1947 to $648 million in the recession year of 1960, an increase of 176 percent.

A steel price increase in the months ahead could shatter the price stability which the country has now enjoyed for some time. In a letter to me on the impact of steel prices on defense costs, Secretary of Defense McNamara states: ‘A steel price increase of the order of $4 to $5 a ton, once its effects fanned out through the economy, would probably raise military procurement costs by $500 million per year or more.’

Steel is a bellwether, as well as a major element in industrial costs. A rise in steel prices would force price increases in many industries and invite price increases in others. The consequences of such a development might be so grave – particularly on our balance of payments position – as to require the adoption of restrictive monetary and fiscal measures which would retard recovery, hold unemployment at intolerable levels, and hamper growth. The depressing effect of such measures on the steel industry's rate of operations might in the long run more than offset the profit-raising effect of a price increase.

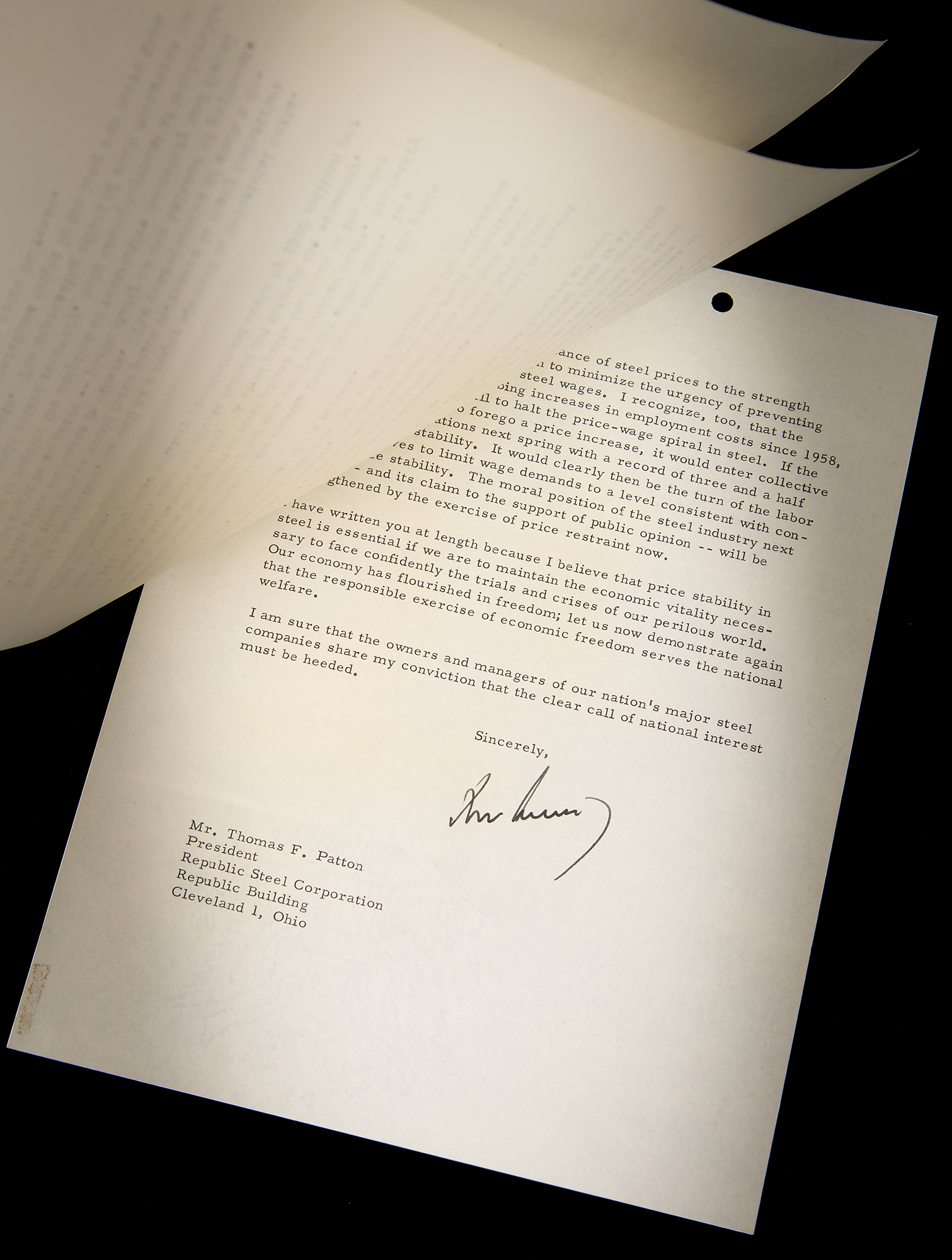

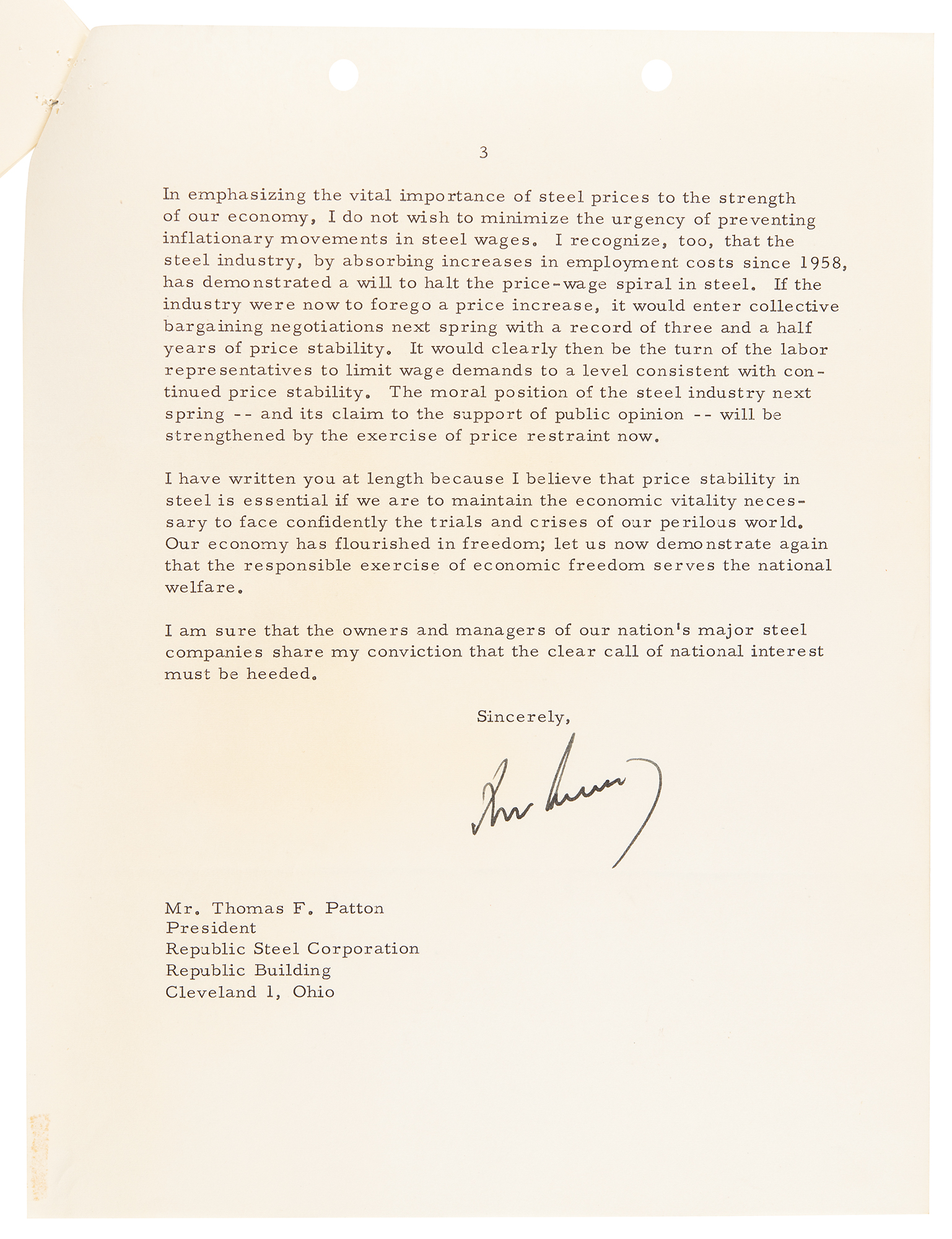

In emphasizing the vital importance of steel prices to the strength of our economy, I do not wish to minimize the urgency of preventing inflationary movements in steel wages. I recognize, too, that the steel industry, by absorbing increases in employment costs since 1958, has demonstrated a will to halt the price-wage spiral in steel. If the industry were now to forego a price increase, it would enter collective bargaining negotiations next spring with a record of three and a half years of price stability. It would clearly then be the turn of the labor representatives to limit wage demands to a level consistent with continued price stability. The moral position of the steel industry next spring – and its claim to the support of public opinion – will be strengthened by the exercise of price restraint now.

I have written you at length because I believe that price stability in steel is essential if we are to maintain the economic vitality necessary to face confidently the trials and crises of our perilous world. Our economy has flourished in freedom; let us now demonstrate again that the responsible exercise of economic freedom serves the national welfare. I am sure that the owners and managers of our nation's major steel companies share my conviction that the clear call of national interest must be heeded.”

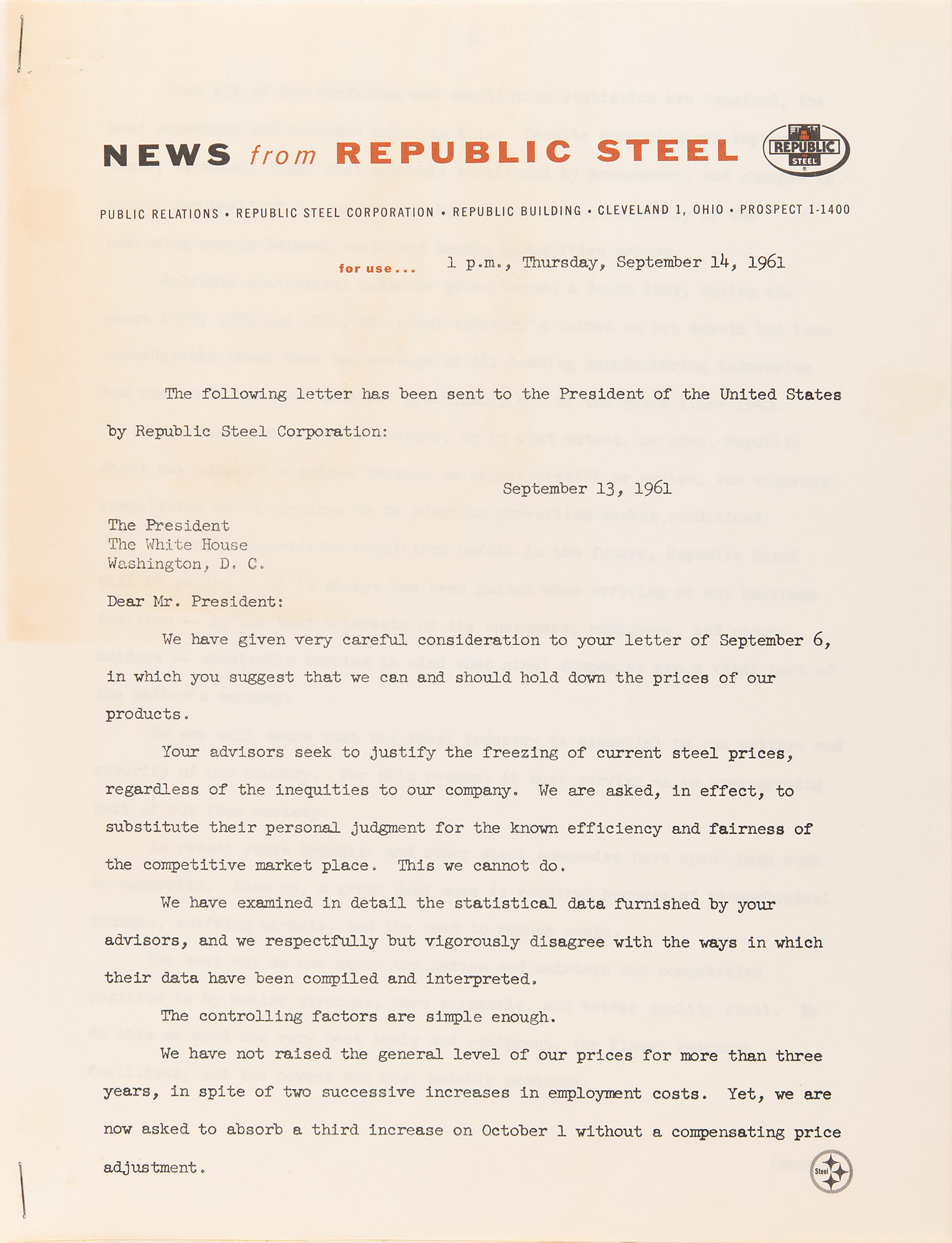

In fine condition, with areas of faint toning, and a small old tape stain to the first page. Accompanied by a copy of Patton’s typed response from September 13, 1961, which politely dismisses the “statistical data furnished by your advisors.” It reads, in part: “We have not raised the general level of our prices for more than three years, in spite of two successive increases in employment costs. Yet, we are now asked to absorb a third increase on October 1 without a compensating price adjustment…

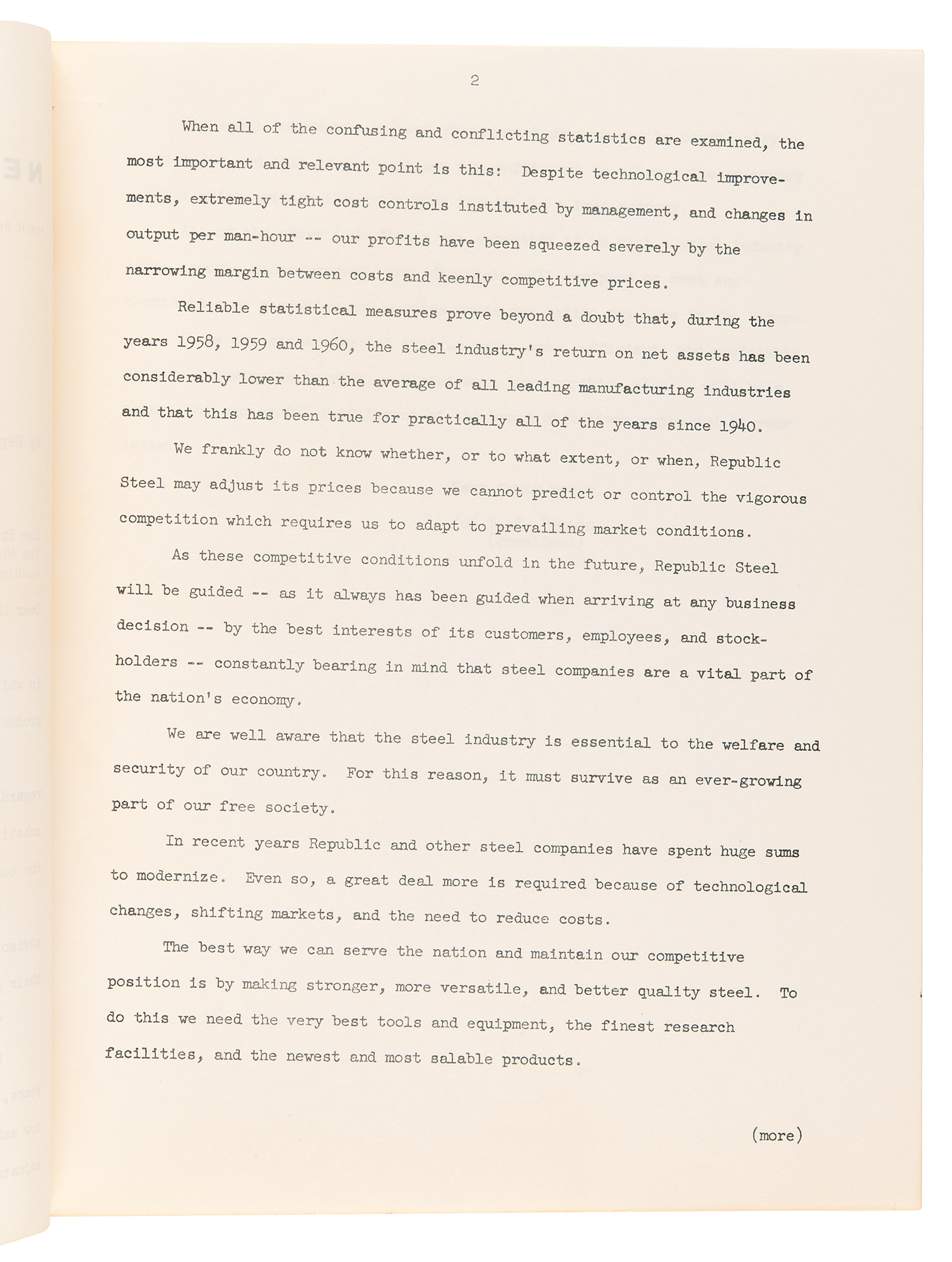

Reliable statistical measures prove beyond a doubt that, during the years 1958, 1959 and 1960, the steel industry's return on net assets has been considerably lower than the average of all leading manufacturing industries and that this has been true for practically all of the years since 1940. We frankly do not know whether, or to what extent, or when, Republic Steel may adjust its prices because we cannot predict or control the vigorous competition which requires us to adapt to prevailing market conditions.

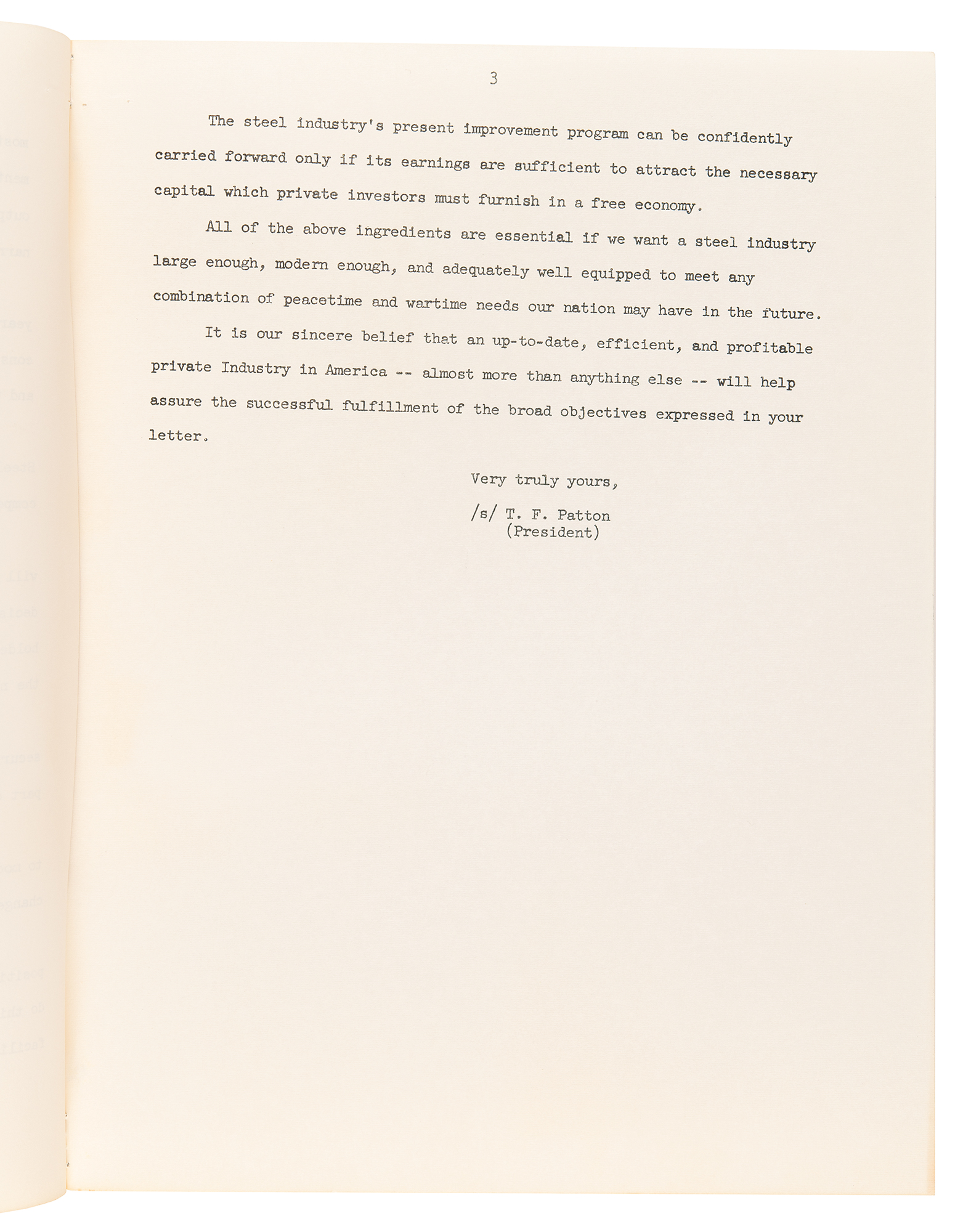

As these competitive conditions unfold in the future, Republic Steel will be guided – as it always has been guided when arriving at any business decision – by the best interests of its customers, employees, and stock-holders – constantly bearing in mind that steel companies are a vital part of the nation's economy…It is our sincere belief that an up-to-date, efficient, and profitable private Industry in America almost more than anything else will help assure the successful fulfillment of the broad objectives expressed in your letter.”

On September 7, 1961, President Kennedy issued a letter to the chief executives of 12 leading steel companies, expressing his strong belief that there was ‘no justification for an increase in steel prices.’ He warned that such an increase could necessitate government intervention in the economy, potentially hindering recovery, increasing unemployment, and impeding economic growth.

Kennedy's administration became actively involved in negotiations with the steel industry and the union to achieve an agreement that would avoid a price hike, particularly given a wage increase scheduled for October 1, 1961. The administration's position was that the wage increase was ‘non-inflationary’ and that rising steel output per man could potentially offset labor costs, making a price increase unnecessary.

Kennedy viewed steel prices as crucial to the strength of the economy, warning that an increase could trigger price increases across various industries and negatively impact the U.S. balance of payments position. Although there was talk of a possible price increase by some industry leaders, no general increase took place in September 1961.

This item is Pre-Certified by PSA/DNA

Buy a third-party letter of authenticity for

$200.00

*This item has been pre-certified by a trusted third-party authentication service, and by placing a bid on this item, you agree to accept the opinion of this authentication service. If you wish to have an opinion rendered by a different authenticator of your choosing, you must do so prior to your placing of any bid. RR Auction is not responsible for differing opinions submitted 30 days after the date of the sale.

Third-party authentication service applies only to signatures and handwriting, and does not cover the addition of sketches, artwork, musical quotations, etc.